If your year-end payroll summary (or W-2 support documents) show substantial overtime, but do not clearly separate the “overtime premium” portion, you may still be able to estimate the qualified amount for the new overtime deduction for Tax Year 2025 (filed in early 2026).

This is not a news post. It is a practical reconstruction method you can apply using your own records. The key concept is simple: only the overtime premium portion (the extra amount above your regular rate required by overtime rules) is what matters for the deduction. Your base pay for those hours is still treated as regular wages.

This guide explains the cleanest shortcut for the most common overtime rate (time-and-a-half) and shows what to save so your numbers are defensible.

Disclaimer: FundFlix.net provides educational information, not tax advice. If your overtime situation is complex (mixed overtime rates, multiple employers, public safety work periods, shift differentials), consider a qualified tax professional and refer to IRS guidance.

Key takeaways

- The overtime deduction applies to qualified overtime compensation under the One Big Beautiful Bill Act (OBBBA) for Tax Year 2025 filings (2026 season), subject to caps and income phaseouts.

- Only the overtime premium portion counts. That is the “extra” pay above your regular rate, not the full overtime wage.

- For standard time-and-a-half (1.5x) overtime, the premium is often one-third of the total overtime pay shown for that rate. That creates the “divide-by-3” shortcut.

- Do not use shortcuts if your overtime rate is not a clean 1.5x or if your overtime is paid at mixed rates (e.g., some 1.5x and some 2.0x). In those cases, you need a proper breakdown.

The core rule: only the premium portion counts

Many people assume “no tax on overtime” means all overtime wages are excluded. That is not how this works.

Overtime pay at time-and-a-half (1.5x) is made of two parts:

- Regular component (1.0x): your normal wages for those hours

- Premium component (0.5x): the extra half-rate on top of normal pay

The deduction is based on the premium component, not the entire overtime amount.

This is why payroll breakdown matters. If your employer reports only a single “overtime pay” number without separating the premium, you must estimate the premium portion yourself using records such as paystubs or payroll summaries.

Who this guide is for (the “yes” list)

You are the intended audience for this method if most of the following are true:

- You are primarily paid hourly (or your pay records clearly identify hourly overtime pay).

- Your overtime is paid at a higher rate than your regular rate (commonly 1.5x).

- Your year-end records show a total overtime pay figure, but do not separately label the premium portion.

Common examples where this often applies:

- Hourly healthcare staff

- Warehouse and manufacturing workers

- Retail and service employees paid hourly

- Skilled trades paid hourly

- Some public safety roles can qualify, but overtime rules can vary due to special work periods, so you must verify the overtime rate and how it is calculated in your case.

Who should not use this shortcut (the “no” list)

Do not use the divide-by-3 shortcut if:

- You are salaried exempt and do not receive overtime premiums under overtime rules.

- Your “extra hours” are paid at straight time (1.0x). If there is no premium, there is nothing to calculate with this method.

- You are a 1099 contractor (gig work). You are not paid overtime premiums under standard overtime rules.

- Your overtime pay is a mix of rates or includes shift differentials and special premiums that are not a simple 1.5x structure.

If any of these apply, you will need a more careful approach (or professional help) instead of shortcuts.

The mechanism: the “divide-by-3” method for standard 1.5x overtime

If your overtime is paid at exactly time-and-a-half (1.5x), the math is straightforward:

Time-and-a-half (1.5x) is:

1.0x regular pay + 0.5x premium

The premium portion (0.5x) is one-third of the total 1.5x amount because:

0.5 / 1.5 = 1/3

That creates a practical shortcut:

Qualified overtime premium (estimate) = Total overtime pay (at 1.5x) ÷ 3

Example

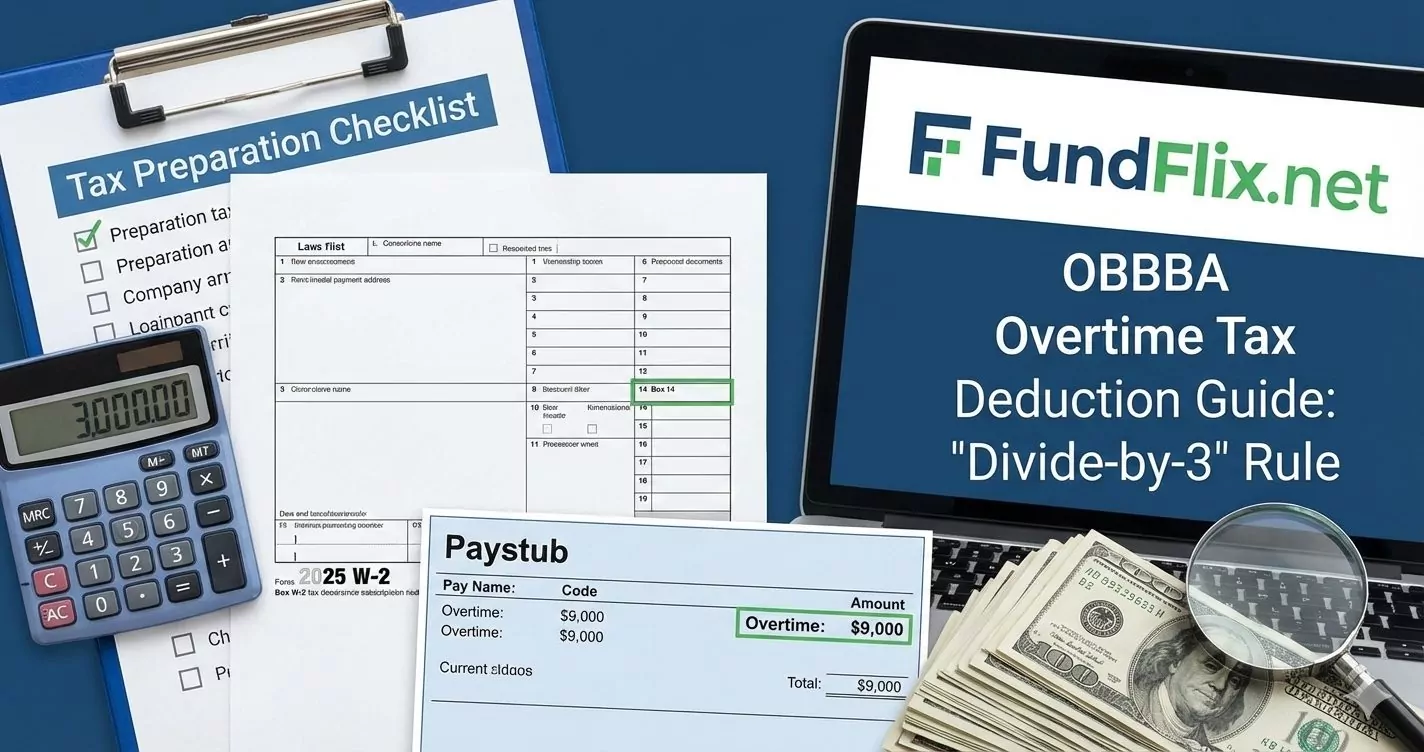

- Your year-end payroll summary shows total overtime pay of $9,000

- You confirm this overtime is paid at 1.5x (time-and-a-half), not mixed rates

- Estimated premium portion: $9,000 ÷ 3 = $3,000

Interpretation:

- The $3,000 is the premium portion estimate

- The remaining $6,000 is the regular component and is treated like normal wages

Important: This shortcut is only valid if the “total overtime pay” number you are using is for overtime paid at 1.5x. If your overtime number mixes 1.5x and 2.0x pay, or includes other premiums, you cannot safely divide by 3.

What about double time (2.0x)?

If your overtime is paid at exactly 2.0x (double time) and the overtime total you are using includes only that rate, the premium portion is typically half the total (because 2.0x = 1.0x + 1.0x premium). However, many people have mixed rates, so treat this as a special case only when you can prove the overtime total is strictly double time.

What records to use (and what to save)

Because you are reconstructing the premium portion, you should keep clean documentation in case your return is questioned.

Minimum “documentation checklist”:

- Final paystub for the year (or a year-end payroll summary) showing year-to-date overtime pay

- A note or screenshot of your method (for example: “Overtime premium estimate = total overtime pay ÷ 3”)

- Any employer payroll report that confirms the overtime rate used (1.5x, 2.0x) and whether the overtime total is separated or mixed

- Your tax software output summary showing where the deduction was placed, so you can reconcile the number later

Keep these records for at least three years, or longer if your situation suggests you should.

Where it goes on your tax return (high-level)

Line placement can vary by tax software and IRS implementation; if unsure, consult a tax professional.

Tax software typically places this deduction on the appropriate line for the qualified overtime deduction based on IRS guidance. The exact line placement can vary by software and IRS implementation details, so the safest approach is:

- Enter the qualified overtime premium amount where your tax software asks for the qualified overtime deduction

- Keep a record of the exact entry screen or worksheet in your software so you can prove how the number was computed and where it was applied

If you are unsure where your software expects this number, use your software’s help panel or consult a tax professional.

How this estimate works (1.5x → divide by 3, 2.0x → divide by 2)

Overtime Premium Estimator

Educational estimate of the overtime FLSA premium portion only. Do not use if your overtime total mixes multiple rates (for example, 1.5x and 2.0x combined) or includes shift differentials/bonuses. If your paystub separately shows an “overtime premium” amount, use that premium figure directly instead of estimating.

Inputs:

- Total overtime pay (YTD)

- Overtime rate selector: 1.5x or 2.0x (with warning about mixed rates)

Outputs:

- Estimated premium portion

- Plain-English explanation of the calculation

- Downloadable worksheet summary (PDF)

Disclaimers:

- Estimates only; user must verify overtime rate and whether totals are mixed

FAQ

My W-2 doesn’t break out overtime. Am I stuck?

Not necessarily. Many payroll systems do not separate items in the way taxpayers expect. If you have reliable payroll records (year-end summary, paystubs) that show your overtime totals and rate, you can estimate the premium portion as shown here for standard 1.5x overtime.

What if I had multiple jobs?

Use the records per employer. Do not combine overtime totals unless you are certain the totals are comparable and you can document the rate for each.

What if my overtime rate changed during the year?

Do not use shortcuts. You need a breakdown by rate or a more careful calculation. Mixed-rate overtime is exactly where people make mistakes.

Is there a cap or income phaseout?

Yes. The deduction is subject to statutory caps and income-based phaseouts. If your income is high, you may be limited or phased out.

Final caution

This method is designed for the most common overtime structure (time-and-a-half) and is meant to help you estimate the premium portion when payroll reporting is not neatly separated. The moment your pay becomes “mixed” (different overtime rates, shift differentials, special pay periods, public safety work cycles), you should slow down and verify your inputs before you claim anything.

If you want FundFlix to turn this into a true “tool page,” the next step is to add the reconstruction worksheet web app and a downloadable worksheet summary so users can save their calculation cleanly.

Related posts:

How High-Income Homeowners Cut Insurance Costs in 2025

How High-Income Homeowners Cut Insurance Costs in 2025

Smart Ways for Fast and Efficient Repayment of Debts

Life Insurance Strategies for Early Retirement (2025 Ultimate Guide)

Lower Luxury Car Insurance by 40% in 2025

Smart Ways for Fast and Efficient Repayment of Debts

Life Insurance Strategies for Early Retirement (2025 Ultimate Guide)

Lower Luxury Car Insurance by 40% in 2025

Financial Risk: What You Should Know

Financial Risk: What You Should Know

This is what you should think about before taking on New Debt

This is what you should think about before taking on New Debt

How to extend a mortgage: everything you need to know

How to extend a mortgage: everything you need to know

How to Use Your Credit Card Wisefully

5 Insurance Hacks to Save Thousands in 2025

High-Net-Worth Insurance Strategies for 2025

How to Use Your Credit Card Wisefully

5 Insurance Hacks to Save Thousands in 2025

High-Net-Worth Insurance Strategies for 2025

Effective Methods for Saving for Retirement: Without Pension Plans

Effective Methods for Saving for Retirement: Without Pension Plans

How to Get The Right Car Loan for Your New Car Purchase

How to Get The Right Car Loan for Your New Car Purchase